Wednesday, April 24, 2024 | St. Lawrence County, NY

Graphics courtesy of New York State comptroller CANTON -- The long-awaited state Comptroller audit of how the Town of Canton’s payroll and finances were handled from 2015 to 2017 was released …

This item is available in full to subscribers.

To continue reading, you will need to either log in to your subscriber account, or purchase a new subscription.

If you are a digital subscriber with an active, online-only subscription then you already have an account here. Just reset your password if you've not yet logged in to your account on this new site.

Otherwise, click here to view your options for subscribing.

Please log in to continue |

Graphics courtesy of New York State comptroller

CANTON -- The long-awaited state Comptroller audit of how the Town of Canton’s payroll and finances were handled from 2015 to 2017 was released Tuesday, Jan. 14, and the analysis calls out the former supervisor, but also the town board on several issues.

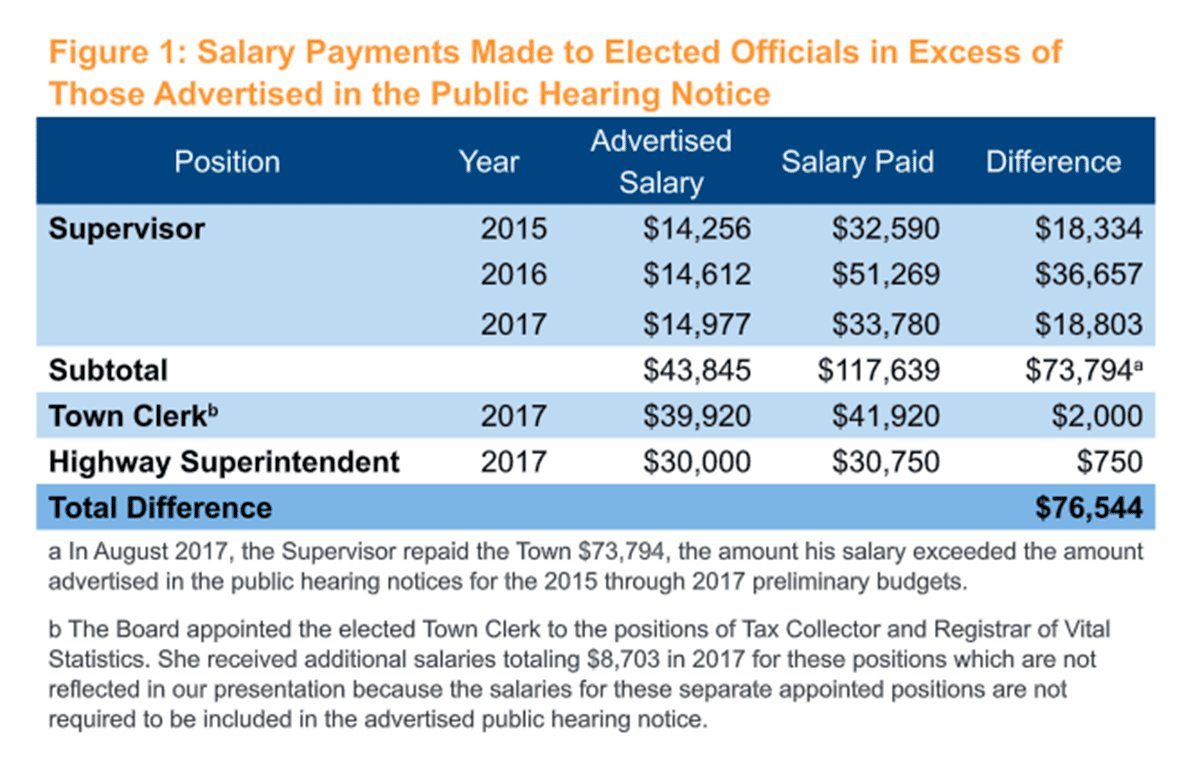

Notably, while the report does criticize former Supervisor David Button for increasing his salary over the legally advertised amount for bookkeeping duties in his office during that time, the audit also zings the elected town board for their lack of oversight concerning the issue.

Another key finding indicates that the board did not authorize additional salaries paid to other elected officials, as well as some health insurance benefits provided by the town.

The audit contains the response to the findings from the town board and current Town Supervisor Mary Ashley. Many of the controls recommended by the state have been implemented since the new supervisor took over in 2018.

The town's receipt of the audit was acknowledged at the town board meeting Wednesday, Jan. 15, however the board did not discuss the findings during the meeting. Copies of the audit are available at the town clerk's office and on the State Comptroller's website.

The town board requested the audit in 2017, after board members at the time began to criticize then Supervisor Button for what they felt was a lack of transparency on how he took over bookkeeping duties in his department after his wife Denise Button’s apparent retirement from the position in 2015, paying himself an additional salary for the work. Mrs. Button continued to work in the office part-time handling some secretarial duties.[img_assist|nid=273360|title=Courtesy of New York State comptroller|desc=|link=none|align=right|width=250|height=278]

Mrs. Button made a small salary to allow her to qualify for worker’s compensation. However, because Button was an elected official, changes in his salary needed to be approved by the town board, a finding backed by the Comptroller’s audit.

After several meetings and numerous public comments critical of the arrangement in 2017, Button paid back the salary he had earned for the bookkeeper’s work since 2015 ($73,794.16) and the town board then approved a payment of $58,857.62 back to Mrs. Button for work she had continued to do after retirement.

The issue, arguably, may have been partly to blame for Button’s loss in the 2017 November election to Mary Ann Ashley, a former village mayor.

Read more on the public and board reaction to the issue here.

“The Supervisor re-allocated the bookkeeper salary to himself and collected additional salaries for bookkeeping duties totaling $73,794 from April 1, 2015 through August 8, 2017 without Board authorization," the Comptroller's audit said.

While the deputy supervisor at the time recalled a discussion regarding the reallocation of the bookkeeper’s salary the other board member did not recall this discussion, the Comptroller’s findings stated.

In addition, town officials were unable to present any evidence to document that the board set the secretary’s salary or authorized the supervisor to increase his salary for the assistant bookkeeper and bookkeeper positions, the audit said. The Comptroller also said that many town officials were not aware of Mrs. Button’s actual retirement in 2015 as the bookkeeper until 2017, and no documentation of an actual retirement was produced.

“OSC has previously expressed the view that the Supervisor may not appoint himself to the position of bookkeeper,” the Comptroller audit said. “If the Supervisor performs bookkeeping functions this must be done in his capacity as Supervisor, not in a separate bookkeeper position. There was no authority for the Supervisor to designate himself as holding the separate position of assistant bookkeeper or bookkeeper and receive a separate salary for these positions.”

However, the Comptroller’s auditors were critical of the town board as well, stating that the board did not pass a local law (subject to permissive referendum) authorizing the increase in the supervisor’s pay in 2015, even though payroll records showed he was collecting the money.

“The town continued to publish the Supervisor’s regular salary in the public notices for the 2016 and 2017 preliminary budgets even though the Supervisor was paid the additional amounts for the bookkeeping work. Although the payroll records showed that the Supervisor was paid the additional salaries as bookkeeper, this was not transparent to the public because the Board did not pass the necessary local laws to allow him to exceed the salaries advertised in the public notices,” the Comptroller said.

The town board’s response in the audit countered this statement by the Comptroller stating: “This paragraph places fault with the Board for failing to properly structure/authorize the increase in the Supervisor’s pay, which pre-supposes that the Board had such knowledge of the increase and would have approved thereof. As stated in numerous other findings in the report, the Board was not made aware of the increase as such it is unknown if the Board would have approved the change.”

The Comptroller’s audit also found that, in addition to the town supervisor, that the clerk and highway superintendent were also paid more than their advertised salaries in the 2015 through 2017 budgets.

“The Town paid the Town Clerk an additional $2,000 salary for duties related to records management,” said the audit. “However, New York State Arts and Cultural Affairs Law provides for the Town Clerk to serve as the Town’s records management officer and these functions are performed in her capacity as Town Clerk.”

The Highway Superintendent was paid $750 more than his advertised salary of $30,000, the Comptroller auditors said. This occurred because the board authorized a 2.5 percent pay increase in 2017 for all town employees. However, the publicly advertised salary for the Highway Superintendent did not take this increase into account, the audit said.

The town responded to this finding stating that because the payments to the Clerk and Highway Superintendent were the responsibility of the former supervisor as the town’s chief fiscal officer to make sure the process was followed properly, that the current board has decided not to seek recovery of the funds.

“To expect the Town Clerk and Highway Superintendent to have to pay back overpayment of funds is fundamentally not fair, nor right, due to the fact that former Town Supervisor David Button did not fulfill the fiduciary duties of the Supervisor of the budget process and legal notification of appropriate salaries,” said the board in their response.

Other findings

Other findings of the Comptroller’s report state that the board did not establish all salaries and wage rates resulting in a total of $145,671 in salaries paid without board authorization, the supervisor’s office did not implement effective payroll controls, heath insurance benefits were not always properly authorized or accurately calculated, and that leave records maintained by the supervisor’s office were not always accurate and available.

The town’s included response to the audit, largely agrees with the findings of the report, besides countering the state’s finding that they should have passed a resolution and approved a local law advertising the salary increase for Mr. Button mentioned earlier in this article.

Town responds

Addressing the Comptroller’s recommendations, the town details changes made since 2018 in how the budget development process is handled in a more transparent way with all board members receiving a tentative budget from the supervisor and then holding budget work sessions open to the public to hash over details. The board also details how the process is advertised to the public and how salaries are disclosed through advertising, legal notices and public meetings.

Other remediation on the town’s part already implemented to address concerns raised in the audit include a more thorough payroll certification process, internal control procedures for postemployment health insurance benefits, a new timesheet system for non-contract employees, the hiring of Gray and Gray CPA to handle the town’s finances and establishing a system to capture and retain employment histories for employees.

Additionally the town plans to “review, re-write and adopt a non-contractual policy in 2020 outlining health insurance benefits, including buy-out options and contribution rates for elected and appointed officials.”

The town also outlines several other changes that have been made since 2018 to further streamline town operations and make town business more transparent, including the closing of 10 superfluous bank town bank accounts and disclosing all personnel additions and changes on public meeting agendas.